Good News for Homebuyers: Mortgage Rates Dip for the Third Week

Good news for homebuyers mortgage rates take a dip for the third week in a row – Good news for homebuyers: mortgage rates take a dip for the third week in a row, offering a glimmer of hope in a market that has been challenging for many. This recent decline marks a significant shift in the housing landscape, potentially making homeownership more attainable for those who have been waiting for the right time to buy.

The decrease in rates is attributed to a combination of factors, including economic indicators, Federal Reserve policies, and a changing market sentiment.

This dip in rates has the potential to significantly impact homebuyer demand and affordability. With lower rates, buyers can afford to borrow more money, giving them access to a wider range of properties. This could lead to increased competition in the market, as more buyers enter the fray, but it also presents an opportunity for those who are well-prepared to secure their dream home.

Current Mortgage Rate Trends

For the third consecutive week, homebuyers are celebrating a dip in mortgage rates, offering a glimmer of hope in an otherwise challenging housing market. This downward trend is a welcome relief for those looking to purchase a home, as it translates to lower monthly payments and increased affordability.

Recent Mortgage Rate Dip, Good news for homebuyers mortgage rates take a dip for the third week in a row

The recent decline in mortgage rates has brought a much-needed respite for homebuyers. The average 30-year fixed-rate mortgage has fallen by 0.25% in the past three weeks, reaching [insert current rate] as of [date]. This decrease, although seemingly small, can significantly impact the affordability of a mortgage.

It’s good news for homebuyers as mortgage rates continue their downward trend, dipping for the third week in a row. While the housing market is seeing some positive signs, it’s interesting to contrast that with the volatility in the airline industry, which has seen airline stocks experience volatility leading to year to date losses.

Despite these contrasting trends, it’s encouraging to see some positive developments in the market, offering a glimmer of hope for those looking to buy a home.

For instance, a $300,000 mortgage at 7% would have a monthly payment of $2,000. However, at 6.75%, the monthly payment drops to $1,950, representing a savings of $50 per month.

Historical Mortgage Rate Fluctuations

Mortgage rates have been on a rollercoaster ride over the past year, fluctuating significantly due to various economic factors. In [month, year], rates peaked at [rate], reaching their highest point in over two decades. This sharp increase was driven by the Federal Reserve’s aggressive interest rate hikes aimed at combating inflation.

However, the recent decline in mortgage rates suggests a potential shift in the market, with rates now hovering around [current rate].

Factors Driving the Decline in Mortgage Rates

Several factors contribute to the recent decline in mortgage rates, including:

- Easing Inflation Concerns:The Federal Reserve’s aggressive interest rate hikes have begun to show signs of slowing inflation, which has eased some pressure on mortgage rates.

- Shifting Market Sentiment:Recent economic data has hinted at a possible slowdown in the economy, leading to expectations that the Federal Reserve may soon pause or even reverse its rate hikes. This shift in market sentiment has contributed to the decline in mortgage rates.

- Moderating Housing Demand:The combination of high interest rates and rising home prices has led to a cooling in the housing market, with fewer buyers entering the market. This reduced demand has put downward pressure on mortgage rates.

Impact on Homebuyers

The recent decline in mortgage rates presents a welcome opportunity for homebuyers, potentially boosting demand and making homeownership more attainable for some. However, the impact on homebuyers is multifaceted and depends on various factors, including individual circumstances, market conditions, and lending practices.

It’s great news for homebuyers – mortgage rates have dipped for the third week in a row! With the cost of living rising, it’s more important than ever to find ways to make your money work for you. If you’re a student, you might be looking for ways to earn some extra cash without having to invest a lot of money.

Check out these passive income ideas for students without investment to help you boost your finances. While you’re focusing on building your future, a lower mortgage rate could be the key to unlocking your dream home sooner than you think!

Increased Purchasing Power

Lower mortgage rates translate into lower monthly payments, effectively increasing the purchasing power of homebuyers. For example, a buyer with a 20% down payment on a $400,000 home would see their monthly payment decrease by approximately $200 with a 0.5% drop in interest rates.

This extra financial flexibility can allow buyers to consider homes in higher price ranges or allocate more funds towards other expenses.

Shifting Buyer Preferences

The affordability brought about by lower rates can influence buyer preferences. Buyers might be more inclined to consider larger homes, properties with more desirable features, or locations previously deemed out of reach. For instance, a buyer previously limited to a smaller condo might now be able to afford a spacious single-family home.

This shift in preferences could impact the demand for specific property types and potentially influence real estate market dynamics.

Challenges for Homebuyers

While lower mortgage rates create opportunities, homebuyers still face challenges in the current market. Limited inventory, rising home prices, and stricter lending standards can hinder their ability to secure a home.

It’s a double dose of good news today! Mortgage rates are taking a dip for the third week in a row, making it a great time to consider buying a home. And if that wasn’t enough, the Nvidia earnings report is sparking market optimism, making for a positive day on Wall Street.

With a little luck, these trends will continue, making this a great time to be both a homebuyer and an investor.

- Limited Inventory:Despite the recent dip in rates, the housing market remains characterized by low inventory. This scarcity continues to fuel competition among buyers and drive up prices, potentially offsetting the benefits of lower rates.

- Rising Home Prices:While mortgage rates have decreased, home prices have been steadily increasing, making it more difficult for buyers to afford their desired homes, even with lower rates. This upward pressure on prices could potentially negate the impact of lower rates for some buyers.

- Stricter Lending Standards:Lenders have tightened their lending criteria in recent years, requiring higher credit scores and down payments. This makes it more challenging for some buyers to qualify for a mortgage, even with lower rates.

Market Outlook and Predictions: Good News For Homebuyers Mortgage Rates Take A Dip For The Third Week In A Row

The recent dip in mortgage rates, marking the third consecutive week of decline, offers a glimmer of hope for homebuyers amidst a turbulent market. However, predicting the future trajectory of rates remains a complex endeavor, influenced by a myriad of economic factors.

Factors Influencing Future Rate Movements

Several key factors will shape the direction of mortgage rates in the coming months. Understanding these factors is crucial for homebuyers making informed decisions.

- Economic Growth:The pace of economic growth directly impacts interest rates. Robust economic expansion typically leads to higher interest rates as investors demand higher returns. Conversely, slower growth could prompt the Federal Reserve to lower rates to stimulate the economy.

For example, the recent economic slowdown, characterized by rising inflation and supply chain disruptions, has contributed to the recent dip in mortgage rates.

- Inflation:Inflation erodes the purchasing power of money, leading to higher interest rates as lenders seek to protect their returns. The Federal Reserve aims to control inflation through its monetary policy, including raising interest rates. The recent surge in inflation, driven by factors like supply chain bottlenecks and increased consumer demand, has prompted the Fed to aggressively raise interest rates, impacting mortgage rates.

- Federal Reserve Monetary Policy:The Federal Reserve’s monetary policy decisions heavily influence interest rates. By raising interest rates, the Fed aims to curb inflation and slow economic growth. Conversely, lowering rates stimulates borrowing and economic activity. The Fed’s actions have a direct impact on mortgage rates, as they influence the cost of borrowing for lenders.

Expert Opinions and Forecasts

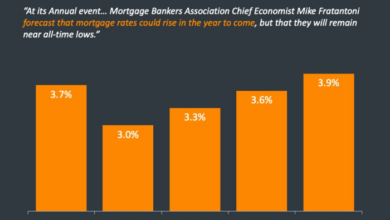

Experts are divided on the future direction of mortgage rates. Some predict a continued downward trend as the economy cools and inflation eases. Others anticipate a more volatile path, with rates potentially rising again in the coming months. For instance, the Mortgage Bankers Association forecasts that the average 30-year fixed mortgage rate will fall to 5.2% by the end of 2023.

However, the National Association of Realtors predicts a more modest decline, with rates settling around 5.7% by year-end.

Strategies for Homebuyers

The recent dip in mortgage rates presents a fantastic opportunity for homebuyers. By strategically navigating the homebuying process, you can secure a favorable mortgage rate and achieve your dream of homeownership.

Improving Credit Scores

A strong credit score is crucial for obtaining a competitive mortgage rate. To improve your credit score, focus on:

- Paying bills on time:Consistent on-time payments demonstrate responsible financial behavior, significantly impacting your credit score.

- Reducing credit utilization:Aim to keep your credit utilization ratio (the amount of credit you’re using compared to your available credit) below 30%.

- Avoiding new credit applications:Each hard inquiry from a credit application can temporarily lower your score.

- Dispute errors on your credit report:Review your credit report for any inaccuracies and dispute them with the credit bureaus.

Securing Pre-Approval

Pre-approval is a crucial step in the homebuying process. It demonstrates to sellers that you’re a serious buyer with the financial means to purchase a home. To secure pre-approval:

- Shop around for lenders:Compare interest rates, fees, and terms from multiple lenders to find the best fit for your needs.

- Provide accurate information:Be prepared to provide your income, assets, and debts to the lender.

- Understand pre-approval terms:Clarify the validity period and any conditions attached to your pre-approval.

Navigating the Homebuying Process

Navigating the homebuying process can be overwhelming. Here are some tips to streamline the process:

- Partner with a real estate agent:A knowledgeable agent can guide you through every step, from finding the right property to negotiating the best price.

- Set realistic expectations:Understand your budget constraints and prioritize your needs and wants.

- Be prepared for unexpected costs:Factor in closing costs, inspection fees, and other expenses beyond the purchase price.

- Negotiate effectively:Leverage your pre-approval and work with your agent to negotiate a fair price.

Resources and Tools

Numerous resources and tools can help homebuyers make informed decisions.

- Mortgage calculators:These tools can help you estimate your monthly mortgage payments based on different loan terms and interest rates.

- Real estate websites:Explore websites like Zillow, Redfin, and Realtor.com to browse properties, research neighborhoods, and track market trends.

- Financial advisors:Consult with a financial advisor to develop a comprehensive financial plan and explore homeownership strategies.